Summary

- Akamai stands to benefit from secular tailwinds such as an increase in e-commerce penetration and online media consumption.

- The company’s security business has also emerged as a major growth driver.

- Investors should consider risks such as the impact of a deep and persistent recession on certain businesses, probability of increasing bad debt, and competitive pressures.

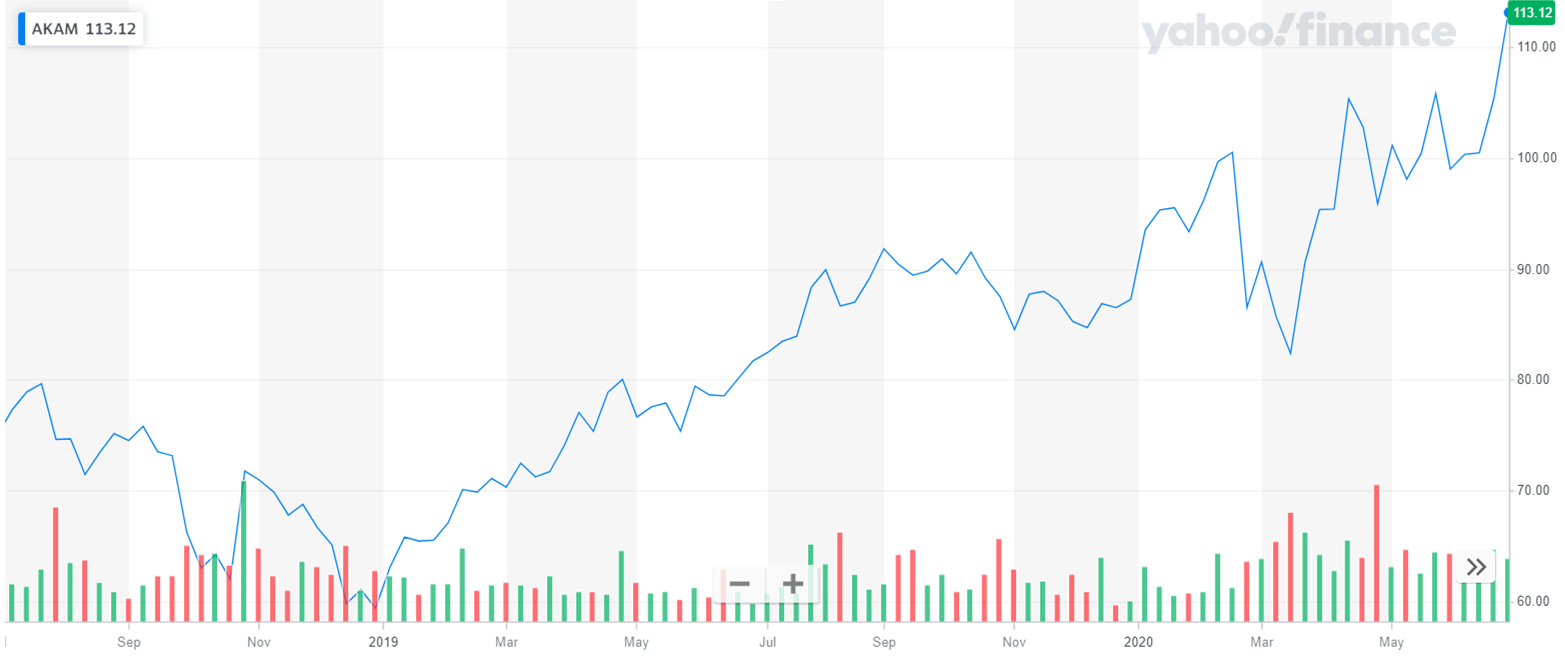

Cloud security and CDN (content delivery network) player Akamai Technologies (NASDAQ:AKAM) seems to have been left behind in what can only be called an enviable rally of the software infrastructure companies. I dare say this even when Akamai itself is trading 30.96% higher on a YTD (year-to-date) basis.

However, these gains look pretty low when we see how competing cloud security and CDN companies have performed in 2020. Peers such as Cloudflare (NET), Limelight Networks (LLNW), and Fastly (FSLY) are up by 113.77%, 90.69%, and 321.08%, respectively, on a YTD basis. Akamai is trading at PS multiple of 6.07x, much lower than the valuation levels of its peers. Here again, Cloudflare and Fastly are trading at staggering PS multiples of 35.45x and 37.74x, respectively. There seems to be no valid reason why Akamai is trading at such a significant discount to its peers, considering the company's scale, profitability, and growth potential.

The Covid-19 pandemic is a big positive for Akamai's media business

The Covid-19 pandemic has forced the entire world to change the way it lives and works. With stay-at-home and work-from-home becoming the new normal, the demand for technology has spiked like never before. Even before the first wave of Covid infections could be completely eradicated, there has been a second wave of infections in some parts of the world. Since an effective and accessible vaccine is expected not before the first half of 2021, people will continue to stay at home for the most part of 2020.

People quarantined at home are consuming media such as VOD (video-on-demand) and gaming services at an alarming pace. Besides solid demand trends, gaming companies are also planning several launches to benefit from the literally captive audience. These trends translated into an almost 30% YoY increase in traffic for the company's platform in a four-week period at the end of the first quarter. The company managed a traffic peak of 167 terabits per second, almost 100% higher than the peak seen in the first quarter of 2019. Akamai prices its customers based on usage and bits delivered, which implies higher traffic translates directly into higher top line growth for the company.

Higher demand for data has triggered the roll-out of various video-streaming services in 2020. This has led to astronomical demand for cloud computing solutions as well as for cloud security solutions. The data has to be transmitted from one place to another in a cheap, bandwidth-efficient, available, and secure manner, which has fueled demand for CDN services.

In the first quarter, Akamai's revenues of $764.3 million grew YoY by 8.18% and were ahead of the consensus by $14.55 million. The company's non-GAAP EPS of $1.2 also beat the consensus by $0.04.