Summary

- PepsiCo has 4% revenue growth but sales by volume are down in several divisions. Operating profit also is down in North American Beverages and Quaker Foods.

- Growing capital expenditures have pushed the price to FY 2019 free cash flow multiple to an uncomfortably high 38. Dividend payout ratio also is trending higher.

- Skepticism is warranted that this spending can produce earnings growth given the challenging environment in the beverage segment.

North American Beverages, Quaker Foods are a Drag

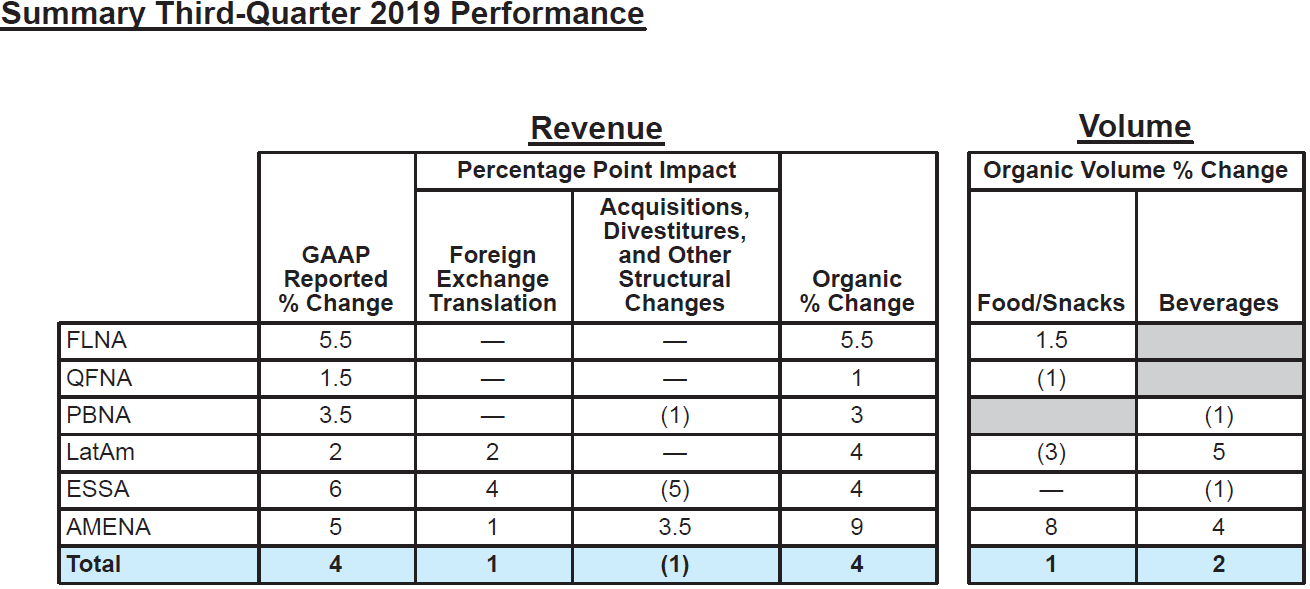

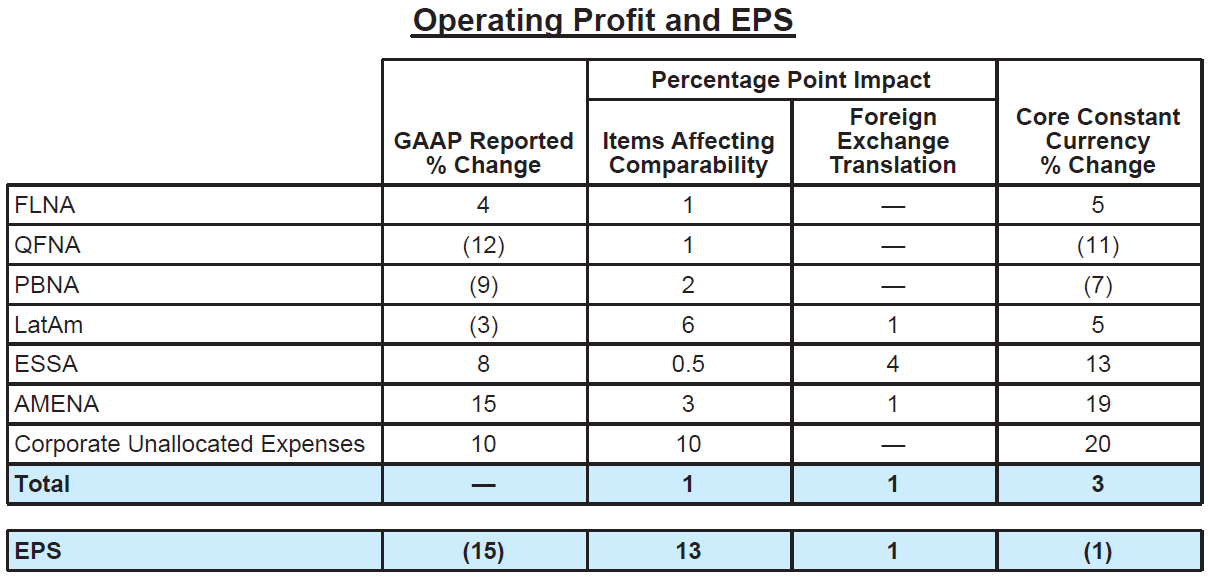

PepsiCo (PEP) just reported 3Q earnings. The company is touting its 4.3% organic revenue growth but volumes only grew 1% in food and 3% in beverages. Operating profit was essentially unchanged, weighed down by the company’s largest division, PepsiCo Beverages North America. While PBNA revenues are up 3.5%, volumes are down 1% and core operating profit is down 7%. Frito Lay North America continues to be the standout division with 5.5% revenue growth. Frito Lay volumes grew by 1.5% and Core Operating Profit increased 5%. The three International segments showed decent growth in both sales and core operating profit, offsetting the declines in PBNA and Quaker Foods.

Source: PepsiCo 3Q 2019 Earnings Release

Source: PepsiCo 3Q 2019 Earnings Release

Higher SG&A (shown on the chart as corporate unallocated expenses) also impacted operating profit. This was driven largely by higher advertising and marketing costs. GAAP net income was lower as the tax rate returned to a more normal 21% this year from an unusually low 7% in 3Q 2018.

Source: PepsiCo 3Q 2019 Earnings Release

Source: PepsiCo 3Q 2019 Earnings Release